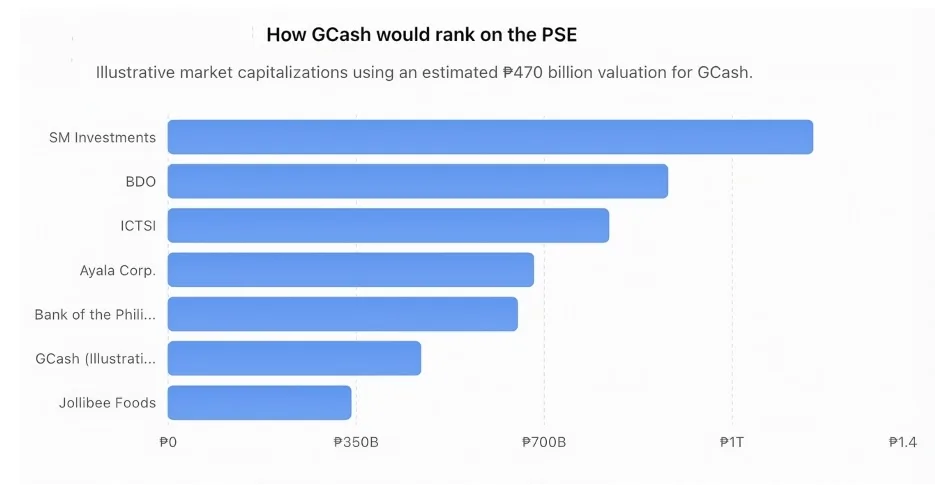

The Philippine Stock Exchange (PSE) is bracing for a massive influx of investors as GCash, the country's dominant digital financial platform, is set to go public with a P470-billion initial public offering (IPO). The listing, which is expected to create a benchmark for future fintech listings, has raised concerns about the PSE's ability to handle the pressure. With a valuation approaching half a trillion pesos, GCash would quickly rank as one of the country's biggest listed companies.

GCash has grown from a text-based money-transfer service in 2004 to a digital financial super application with about 94 million registered users. Its parent company, Mynt, is aiming for a valuation of at least $8 billion through the offering, while raising about $1 billion. Investors are not just buying a payments company; they are buying a platform with a future increasingly reliant on consumer finance, wealth management, and digital banking.

But not all outstanding companies make an outstanding IPO. The key issue is whether the Philippine capital market has the capacity to accommodate a company of this size without disrupting the rest of the exchange. At a valuation approaching half a trillion pesos, GCash would compete with businesses that have spent decades constructing banks, power plants, property portfolios, and infrastructure assets. Unlike those traditional companies, however, GCash's valuation rests primarily on future growth rather than accumulated physical assets.

The PSE remains one of Asia's illiquid markets, with daily trading activity concentrated in a limited number of blue-chip stocks. Foreign investors have been significant net sellers in recent years, and finite pools of capital are held by domestic pension funds, insurance companies, and mutual funds. This means that unless the IPO raises substantial new foreign funds, demand for GCash shares is likely to originate from investors selling existing investments.

A successful GCash listing could broaden investor choice, but it could also divert scarce investment capital away from Philippine corporations already competing for limited liquidity. The more attractive the GCash story becomes, the greater the potential rotation from established blue chips. Valuation presents another challenge, with an $8 billion valuation implying an extraordinary premium for future earnings growth.

The actual investment case for GCash is not in payments but in monetization. Payments businesses process enormous transaction volumes while earning relatively thin margins. Real profits come from higher value-added operations such as consumer lending, insurance distribution, investment products, and merchant financing. GCash has cleverly diversified into all these offerings, transforming from a mere e-wallet into a strong digital financial ecosystem.

The listing is expected to be a referendum on the maturity of the Philippine capital market, with experts warning that failure could reveal structural weaknesses. The question is whether the PSE can handle the pressure and provide the liquidity needed to support a company of this size. Only time will tell.