The Bureau of Internal Revenue (BIR) just dropped a circular that foreign digital service providers won't like — and local businesses can't ignore.

On June 18, 2026, the BIR issued Revenue Memorandum Circular (RMC) No. 59-2026, spelling out exactly who pays what under the new VAT on digital services law. The short version: foreign companies selling digital services to Filipinos must collect 12% VAT, just like local businesses do.

The law itself — Republic Act No. 12023, backed by Revenue Regulations No. 3-2025 — has been rolling out since last year. But RMC No. 59-2026 answers the tricky questions that businesses have been asking, especially about cross-border transactions and tax treaties.

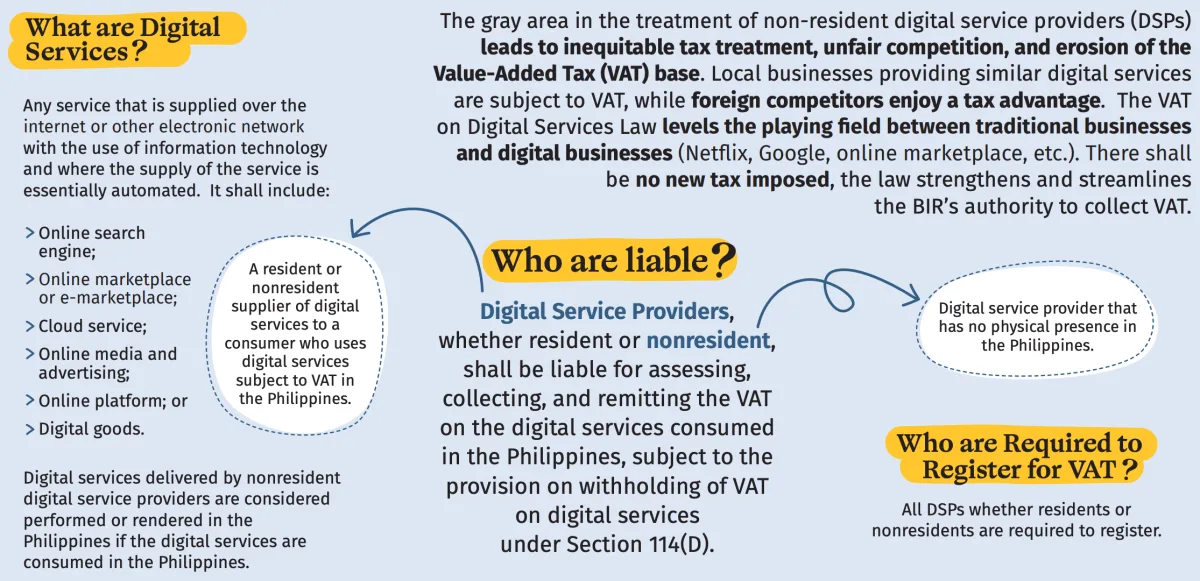

Here's the headline: non-resident digital service providers (NRDSPs) — think streaming platforms, cloud services, online advertising, and app stores — are liable for VAT if their services are consumed in the Philippines. But how the tax is collected depends on who the customer is.

If the customer is a regular person — a B2C transaction — the foreign provider must register with the BIR, charge 12% VAT, remit it, and file VAT returns. That means Netflix, Spotify, and Google Play must handle the tax themselves for individual Filipino users.

But if the customer is a Philippine business — a B2B transaction — the responsibility shifts. The local business must withhold the VAT from the payment to the foreign provider and remit it directly to the BIR using a reverse charge mechanism. So if your company buys cloud storage from a foreign provider, you're the one who needs to file the VAT return.

Even NRDSPs that only sell VAT-exempt digital services — like educational content or certain financial services — still have to register with the BIR and file returns. They just report their exempt sales as zero-rated.

And here's the part that will frustrate tax lawyers: you can't use tax treaties to dodge VAT. The BIR made it clear that VAT is a consumption tax, not an income tax. Tax treaties — which cover things like business profits, royalties, and dividends — don't apply. So even if a foreign company has a treaty benefit for income tax, it still owes VAT on digital services consumed in the Philippines.

What about cost-sharing arrangements? Say a foreign parent company buys digital services for itself and its Philippine subsidiary. If the foreign company doesn't directly sell to the Philippine subsidiary, the foreign affiliate is considered the NRDSP and must register. The local subsidiary doesn't get a free pass.

Why does this matter? Before RA 12023, local businesses had to charge 12% VAT on their services, but foreign competitors didn't. That gave giants like Google and Meta a pricing advantage over local digital advertisers and content providers. The BIR says the law is meant to level the playing field — and RMC No. 59-2026 makes sure no one slips through the cracks.

For Filipino consumers, this likely means higher prices on streaming subscriptions and app purchases — the VAT will be added to the bill. For local businesses buying software or cloud services from abroad, it means new compliance work: registering as a VAT-withholding agent and filing extra returns.

"Treaty provisions generally cannot be invoked to exempt NRDSPs from VAT obligations," the BIR clarified in RMC No. 59-2026.

Mon Abrea, a global tax policy expert and chief tax advisor at the Asian Consulting Group, broke down the circular in a Rappler column. He noted that the BIR is serious about enforcement and that companies should consult tax advisors to avoid penalties.

The circular is effective immediately. Foreign digital service providers that haven't registered yet are now on notice. Local businesses that buy from unregistered NRDSPs should check their contracts — because the withholding obligation falls on them.

- Law: Republic Act No. 12023 (VAT on Digital Services), effective 2025

- VAT rate: 12% on digital services consumed in the Philippines

- B2C: Foreign provider registers, collects, and remits VAT

- B2B: Local business withholds and remits VAT via reverse charge

- Tax treaties: Don't exempt NRDSPs from VAT

- Registration required even for VAT-exempt services

- RMC No. 59-2026 issued June 18, 2026, clarifying RMC No. 47-2025