Ayala Land Inc. just got a brutal downgrade from First Metro Securities — target price slashed by nearly 45%, stock rating cut to “hold.” But one veteran analyst says the market is confusing a rough patch with a collapse.

The downgrade points to slowing residential sales, rising debt maturities, negative free cash flow, and the risk of being kicked out of the MSCI Philippines Standard Index. Those are real problems. But are they enough to treat one of the country’s premier real estate franchises as a structurally broken business?

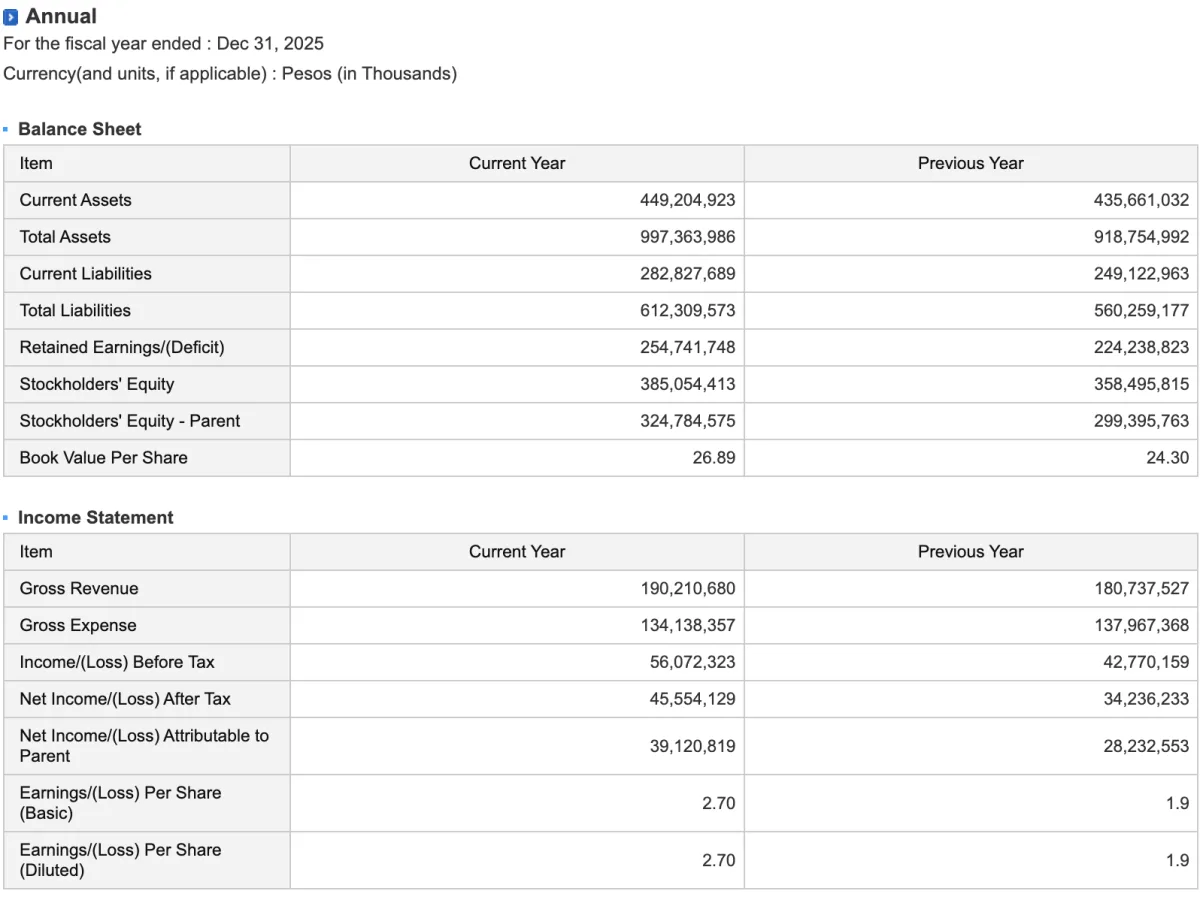

A forensic read of Ayala Land’s financials suggests otherwise. The company generated P190.2 billion in revenues in 2025 and P39.1 billion in reported net income — a 39% jump year-on-year. Strip out one-off gains, and core net income still grew 8% to P30.6 billion. Those aren't the numbers of a company in distress.

Bears will point to the free cash flow deficit that has widened in recent years and the P74 billion in debt maturing over the next 12 months. Those concerns are legitimate. But context matters. In real estate development, free cash flow is typically negative when you're buying land and funding construction. The real question is whether those upfront costs build assets that will generate earnings for years.

Ayala Land’s balance sheet shows P1 trillion in assets — townships, commercial hubs, industrial complexes, offices, hotels, and residential centers. These are some of the most valuable real estate holdings in the country. The company also has P325 billion in equity and constant access to local capital markets. That isn't a company facing a liquidity crisis.

What's more sobering is Ayala Land’s decision to scale back 2026 capital spending to around P50 billion. That's a mark of conservatism, not panic.

Still, the headwinds are real. Residential development remains Ayala Land’s biggest earner, but it's under stress. Rising interest rates, lower affordability, and slower inventory turnover have hit demand across the industry. First-quarter 2026 results showed revenues falling to P37.5 billion and net income dropping to P5.4 billion. Property development revenues fell 27% year-on-year.

What the bearish narrative misses, the analyst argues, is that Ayala Land is no longer just a residential developer. Over the past two decades, it has transformed into a diversified property platform. Malls, offices, hotels, industrial parks, logistics facilities, and mixed-use townships now account for a large portion of the business. These recurring-income assets keep producing cash flow even when condo sales slow.

“Markets tend to get most optimistic near the top of a cycle and most pessimistic near the bottom.”

The analyst, drawing on nearly three decades of experience, says First Metro’s report raises legitimate concerns but that the numbers tell a different story. The real risk isn't that Ayala Land is in decline — it's that the market is pricing in a permanent downturn when the company is just navigating a cycle.